2026 Housing Market Forecast: 3% Price Dip Analysis

The real estate landscape is perpetually in motion, influenced by a myriad of economic, social, and political factors. As we cast our gaze towards the future, specifically the 2026 Housing Market, a key projection has emerged: a potential 3% dip in home prices. This forecast, while seemingly modest, carries significant implications for everyone involved in real estate, from first-time homebuyers to seasoned investors, and from individuals looking to sell their cherished homes to those navigating the complexities of property development. Understanding the nuances of this predicted shift is crucial for making informed decisions and strategically positioning oneself in a dynamic market.

For years, many regions have experienced unprecedented appreciation in home values, driven by low interest rates, limited inventory, and robust demand. However, the economic tides are always turning, and what goes up often experiences periods of recalibration. A 3% dip, while not a crash, signals a potential cooling period, offering both challenges and opportunities. This comprehensive analysis will delve into the factors contributing to this forecast, explore its potential impact on various market participants, and provide actionable strategies to navigate the evolving 2026 Housing Market.

Understanding the 2026 Housing Market Forecast: What’s Driving the 3% Dip?

Before we can fully grasp the implications of a 3% dip in home prices, it’s essential to dissect the underlying forces that are likely to shape the 2026 Housing Market. Several interconnected economic indicators and market dynamics are at play, each contributing to the anticipated shift.

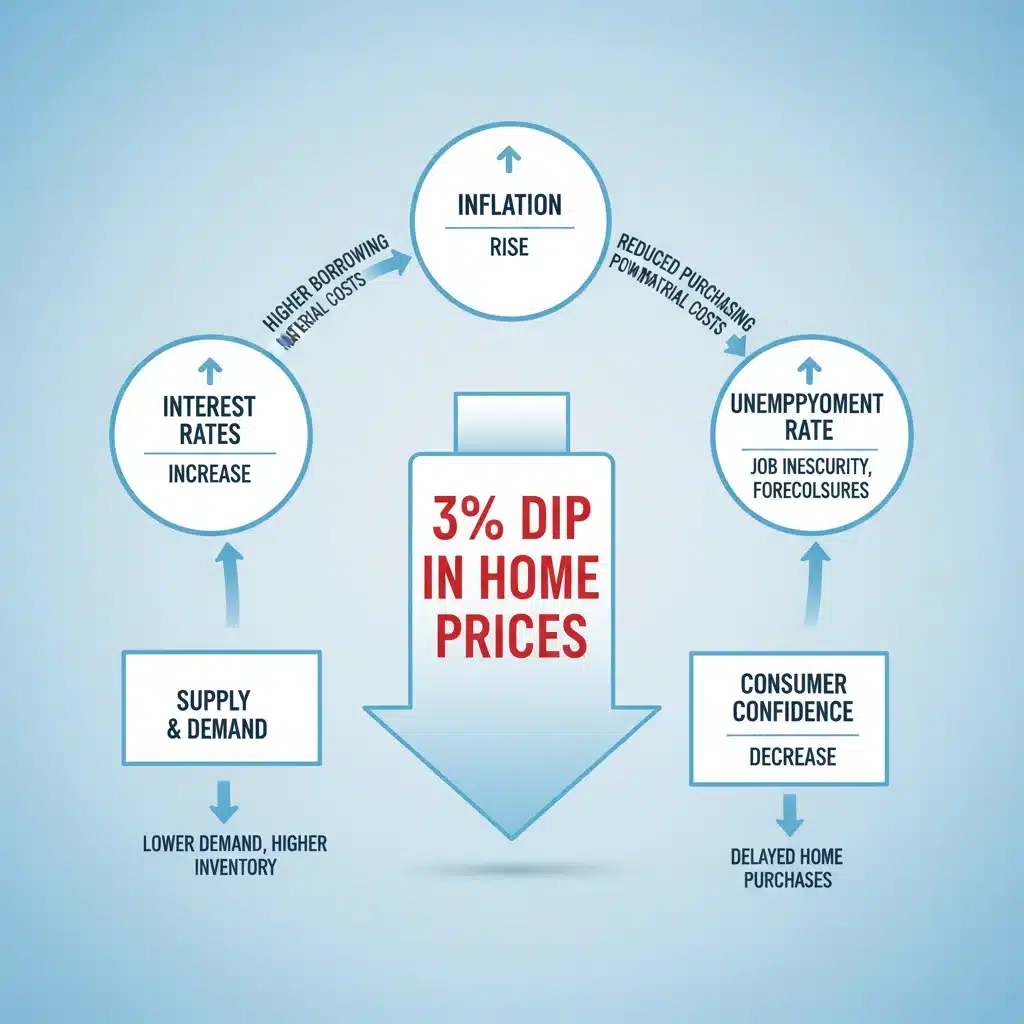

Interest Rate Trajectories

One of the most significant levers in the housing market is interest rates. The Federal Reserve’s monetary policy, aimed at managing inflation and economic stability, directly impacts mortgage rates. Historically, periods of rising interest rates tend to cool down housing demand as borrowing becomes more expensive, reducing buyers’ purchasing power. While the exact trajectory of interest rates leading up to 2026 is subject to ongoing economic developments, a sustained period of higher rates could certainly contribute to a modest price correction.

Inflation and Economic Growth

Inflation, a persistent concern in recent times, also plays a crucial role. While central banks aim to bring inflation under control, its lingering effects can erode consumer confidence and discretionary spending. A slowdown in overall economic growth, perhaps due to tighter monetary policies or global economic headwinds, could also temper demand for housing. Conversely, if inflation cools significantly, it might allow for more stable interest rates, potentially softening the dip or even stabilizing prices sooner. The delicate balance between controlling inflation and fostering sustainable economic growth will be a key determinant for the 2026 Housing Market.

Supply and Demand Dynamics

The fundamental principles of supply and demand remain paramount. For years, many markets have grappled with a severe shortage of housing inventory, which has propelled prices upward. While construction activity has increased in some areas, it often struggles to keep pace with demographic shifts and household formation. However, if rising interest rates or economic uncertainty lead to a decrease in buyer demand, even a relatively stable supply could create an imbalance, leading to a slight oversupply in certain segments and contributing to the 3% price dip. Furthermore, a potential increase in sellers, perhaps due to changing life circumstances or a desire to capitalize on previous gains before further corrections, could also add to inventory levels.

Demographic Shifts and Migration Patterns

Demographics are a powerful, albeit slower-moving, force in real estate. The aging of the baby boomer generation, the rise of millennials entering their prime homebuying years, and the evolving preferences of Generation Z all influence housing demand. Migration patterns, driven by job opportunities, affordability, and lifestyle choices, also play a significant role. If certain regions experience out-migration or a slowdown in new household formation, this could exert downward pressure on prices in those specific areas, contributing to the national average dip.

Affordability Challenges

Years of rapid price appreciation, coupled with rising interest rates, have created significant affordability challenges for many prospective buyers. This is particularly true for first-time homebuyers and those in lower-income brackets. At a certain point, housing prices can become disconnected from local income levels, creating a ceiling for further growth. A 3% dip could be a natural market correction to bring prices back into closer alignment with what a larger segment of the population can reasonably afford, thus fostering a more sustainable 2026 Housing Market.

Implications for Buyers in the 2026 Housing Market

A 3% dip in home prices in the 2026 Housing Market presents a nuanced landscape for buyers. While it might not represent a dramatic ‘buyer’s market’ in the traditional sense, it certainly shifts the balance of power more favorably towards those looking to purchase.

Increased Affordability (Slightly)

The most direct benefit for buyers is the potential for increased affordability. A 3% reduction in price, while not enormous, can translate to thousands of dollars saved on the purchase price, and consequently, a slightly lower monthly mortgage payment (assuming interest rates remain stable). For buyers who have been priced out of the market, this small shift could be enough to bring certain properties within reach, especially in conjunction with other favorable conditions.

Less Competition and More Negotiation Power

In a market where prices are dipping, even marginally, sellers may become more amenable to negotiations. This could mean fewer bidding wars, more opportunities to include contingencies (like home inspections and appraisals) without fear of being outbid, and potentially negotiating on closing costs or repair credits. Buyers might find themselves with more time to make decisions and less pressure to waive crucial protections. This is a significant change from the highly competitive markets of recent years.

Strategic Timing for Entry

For patient buyers, the 2026 Housing Market could offer a strategic entry point. While it’s impossible to perfectly time the market, a period of slight price correction can reduce the risk of overpaying at the peak. Buyers who have saved diligently and are pre-approved for a mortgage might find themselves in a strong position to acquire property at a more reasonable valuation. It’s crucial, however, to focus on long-term investment goals rather than trying to catch the absolute bottom.

Importance of Due Diligence

Even with a slight price dip, thorough due diligence remains paramount. Buyers should continue to work with experienced real estate agents, obtain comprehensive home inspections, and carefully review all documentation. Understanding local market conditions, even within a national trend, is vital as real estate is inherently local. Some micro-markets might experience greater corrections, while others remain more resilient.

Implications for Sellers in the 2026 Housing Market

For sellers, a 3% dip in home prices in the 2026 Housing Market necessitates a recalibration of expectations and a more strategic approach to listing their properties. The days of multiple, over-asking-price offers within hours of listing may become less common.

Realistic Pricing is Key

The most critical adjustment for sellers will be adopting a realistic pricing strategy. Overpricing a home in a cooling market can lead to prolonged listing times, price reductions, and ultimately, a lower selling price than if it had been priced appropriately from the outset. Sellers should rely on current comparable sales (comps) and their real estate agent’s expertise to set a competitive and attractive price, rather than basing it on peak market values from previous years.

Enhanced Presentation and Marketing

In a market with more inventory and less frenzied demand, presentation matters more than ever. Sellers should invest in professional staging, high-quality photography, and compelling marketing materials to make their property stand out. Addressing minor repairs, decluttering, and ensuring the home is move-in ready can significantly improve its appeal and reduce the likelihood of buyers seeking large concessions.

Flexibility in Negotiations

Sellers in the 2026 Housing Market should be prepared for more negotiation. This could involve being open to offers below the asking price, contributing to closing costs, or agreeing to certain repairs. Flexibility can be the difference between a successful sale and a property languishing on the market. Understanding the buyer’s perspective and being willing to compromise can facilitate a smoother transaction.

Consider Your Equity and Long-Term Goals

For many sellers, particularly those who purchased before the recent boom, a 3% dip will still leave them with significant equity. It’s important to consider your long-term financial goals. If you’re selling to downsize, relocate, or upgrade, the slight dip might be offset by a more favorable purchase price on your next home. Consulting with a financial advisor can help assess the overall impact on your personal financial situation.

Strategies for Navigating the 2026 Housing Market

Whether you’re buying, selling, or investing, proactive strategies are essential to thrive in the anticipated 2026 Housing Market. Adaptation and informed decision-making will be your greatest assets.

For Buyers:

- Get Pre-Approved (and Re-Approved): Understand your borrowing capacity and lock in the best possible interest rate. Revisit your pre-approval regularly as rates can fluctuate.

- Be Patient but Prepared: While the market may cool, desirable properties will still attract attention. Be ready to act when the right home comes along, but don’t rush into a decision.

- Focus on Long-Term Value: Look beyond short-term price fluctuations. Consider the property’s location, potential for appreciation over time, and how it fits your lifestyle goals.

- Leverage Professional Guidance: Work with a seasoned real estate agent who understands local market trends and can provide expert advice on pricing, negotiations, and market dynamics.

- Inspect Thoroughly: Do not waive home inspections. A detailed inspection can uncover costly issues and provide leverage for negotiations.

For Sellers:

- Price Strategically: Avoid overpricing. Consult with your agent to set a competitive price based on current market conditions, not past peaks.

- Enhance Curb Appeal & Interior: First impressions matter. Invest in minor repairs, fresh paint, decluttering, and professional staging to maximize your home’s appeal.

- Be Flexible and Responsive: Be open to negotiations on price, contingencies, and closing dates. A quick and smooth transaction can be more valuable than holding out for a top-dollar offer that never materializes.

- Market Aggressively: Utilize professional photography, virtual tours, and a strong online presence to reach a wider audience.

- Understand Your Equity Position: Work with a financial advisor to understand your net proceeds after selling and how it aligns with your future financial plans.

For Investors:

The 2026 Housing Market, with its predicted 3% dip, could present interesting opportunities for investors, particularly those with a long-term perspective.

- Identify Undervalued Assets: A cooling market can reveal properties that are genuinely undervalued, especially if sellers are motivated.

- Focus on Cash Flow: For rental property investors, strong rental demand and positive cash flow remain critical. Research local rental markets thoroughly.

- Consider Fix-and-Flip Opportunities: While potentially riskier in a dipping market, properties requiring renovation might offer higher profit margins if purchased at a discount and renovated efficiently.

- Diversify Your Portfolio: Don’t put all your eggs in one basket. Consider diversifying across different property types or geographic locations to mitigate risk.

- Stay Informed on Local Regulations: Rental laws, zoning changes, and property taxes can significantly impact investment returns.

The Broader Economic Context Beyond the 2026 Housing Market

It’s important to remember that the 2026 Housing Market does not exist in a vacuum. Broader economic trends will continue to exert significant influence. Global geopolitical events, technological advancements, and shifts in employment sectors can all have ripple effects on consumer confidence, job growth, and ultimately, housing demand.

Geopolitical Stability

International conflicts or significant global economic disruptions can introduce uncertainty, causing investors to pull back and consumers to become more cautious. Such events could either exacerbate a housing market slowdown or, in some cases, drive demand for safe-haven assets, including real estate in stable economies.

Technological Advancements

The rise of remote work, accelerated by recent global events, has fundamentally altered where and how people choose to live. This trend is likely to continue evolving, impacting demand in urban centers versus suburban and rural areas. Smart home technology and sustainable building practices are also shaping buyer preferences and property values, adding another layer of complexity to the 2026 Housing Market.

Employment and Wage Growth

A healthy labor market with consistent wage growth is a strong underpinning for housing demand. If employment remains robust and wages continue to increase, it can help offset the impact of higher interest rates and maintain overall affordability, even with a slight price dip. Conversely, a significant increase in unemployment could put further downward pressure on home prices.

Conclusion: Navigating the Nuances of the 2026 Housing Market

The forecast of a 3% dip in home prices for the 2026 Housing Market is not a cause for panic, but rather a call for strategic planning and informed action. It represents a potential return to a more balanced market, moving away from the frenetic pace and rapid appreciation seen in recent years. For buyers, it could mean a slightly more accessible entry point and greater negotiating power. For sellers, it emphasizes the importance of realistic pricing, strong presentation, and flexibility.

Ultimately, success in the 2026 Housing Market will hinge on understanding the interplay of economic forces, recognizing local market specificities, and engaging with experienced real estate professionals. Whether you are looking to buy your first home, sell an existing property, or expand your investment portfolio, staying informed and adapting your strategy will be paramount. The real estate journey is rarely linear, and while a 3% dip might signal a slight detour, it also paves the way for new opportunities for those prepared to seize them.

By focusing on long-term goals, exercising due diligence, and embracing flexibility, both buyers and sellers can navigate the evolving landscape of the 2026 Housing Market with confidence and emerge successfully positioned for the future.