Student Loan Repayment Options for 2026 Graduates: A Detailed Overview

Student Loan Repayment Options for 2026 Graduates: A Detailed Overview

Congratulations, Class of 2026! As you prepare to embark on your professional journeys, a significant financial milestone awaits: managing your student loans. The landscape of student loan repayment can seem daunting, but with the right knowledge and strategic planning, you can navigate it successfully. This comprehensive guide is specifically tailored for 2026 graduates, offering a detailed overview of the various student loan repayment options available, both federal and private, along with expert tips to help you make informed decisions.

Understanding your student loan repayment obligations is not just about making monthly payments; it’s about building a solid financial foundation for your future. The decisions you make now can impact your credit score, your ability to purchase a home, and your overall financial well-being for years to come. Therefore, taking the time to thoroughly explore all your options is paramount. We’ll delve into the nuances of federal loan programs, including income-driven repayment plans, and also touch upon strategies for managing private student loans. Our goal is to equip you with the knowledge to confidently approach your student loan repayment journey.

The Basics: Federal vs. Private Student Loans

Before diving into specific repayment plans, it’s crucial for 2026 graduates to understand the fundamental differences between federal and private student loans. This distinction will heavily influence the repayment options available to you.

Federal Student Loans

Federal student loans are issued by the U.S. Department of Education and come with a range of benefits and protections not typically found with private loans. These include:

- Fixed Interest Rates: Interest rates are set by Congress and remain constant for the life of the loan.

- Income-Driven Repayment (IDR) Plans: Payments can be adjusted based on your income and family size.

- Loan Forgiveness Programs: Opportunities for loan forgiveness exist for certain professions or after a specified period of payments.

- Deferment and Forbearance Options: Ability to temporarily postpone payments during periods of financial hardship.

- No Credit Check (for most undergraduate loans): Often don’t require a credit check or co-signer for undergraduates.

Common types of federal loans include Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans (for graduate students and parents), and Direct Consolidation Loans.

Private Student Loans

Private student loans are offered by banks, credit unions, and other private lenders. They typically:

- Have Variable or Fixed Interest Rates: Variable rates can fluctuate, potentially increasing your monthly payments.

- Require a Credit Check and Often a Co-signer: Eligibility is often based on creditworthiness.

- Offer Fewer Repayment Protections: Generally lack the flexible repayment plans, deferment options, and forgiveness programs of federal loans.

- May Have Different Fees: Origination fees and late payment fees can vary widely.

It’s important to identify which type of loans you hold, as this will dictate your available student loan repayment 2026 strategies.

Standard Federal Student Loan Repayment Plans

For most federal student loan borrowers, repayment automatically begins six months after you graduate, leave school, or drop below half-time enrollment. This is known as the grace period. During this period, interest may accrue on some types of loans. Once your grace period ends, your loans will typically enter the Standard Repayment Plan unless you actively choose another option.

1. Standard Repayment Plan

This plan is the default for most federal student loans. You’ll pay a fixed amount each month for up to 10 years (or up to 30 years for Direct Consolidation Loans). The Standard Repayment Plan is designed to pay off your loan in the shortest amount of time, resulting in the least amount of interest paid over the life of the loan. While the monthly payments are higher than some other plans, it’s often the most cost-effective option if you can afford it.

2. Graduated Repayment Plan

Under this plan, your payments start lower and gradually increase, usually every two years. The repayment period is still typically 10 years (or up to 30 years for Direct Consolidation Loans). This plan can be helpful if you expect your income to increase over time, making the initial lower payments more manageable. However, you will pay more in total interest compared to the Standard Repayment Plan.

3. Extended Repayment Plan

If you have more than $30,000 in federal student loans, you may be eligible for the Extended Repayment Plan. This plan allows you to make either fixed or gradually increasing payments for up to 25 years. While this significantly lowers your monthly payment, it also means you’ll pay substantially more in total interest over the longer repayment period.

Income-Driven Repayment (IDR) Plans: A Lifeline for Many 2026 Graduates

For many 2026 graduates, especially those entering fields with lower starting salaries or facing economic uncertainty, Income-Driven Repayment (IDR) plans can be a game-changer. These plans calculate your monthly payment based on your discretionary income and family size, rather than your loan balance. This can make your payments much more affordable. After a certain number of years (20 or 25, depending on the plan), any remaining loan balance may be forgiven, though the forgiven amount might be taxable income.

There are several types of IDR plans, and it’s essential to understand the nuances of each to determine which one is best for your student loan repayment 2026 strategy:

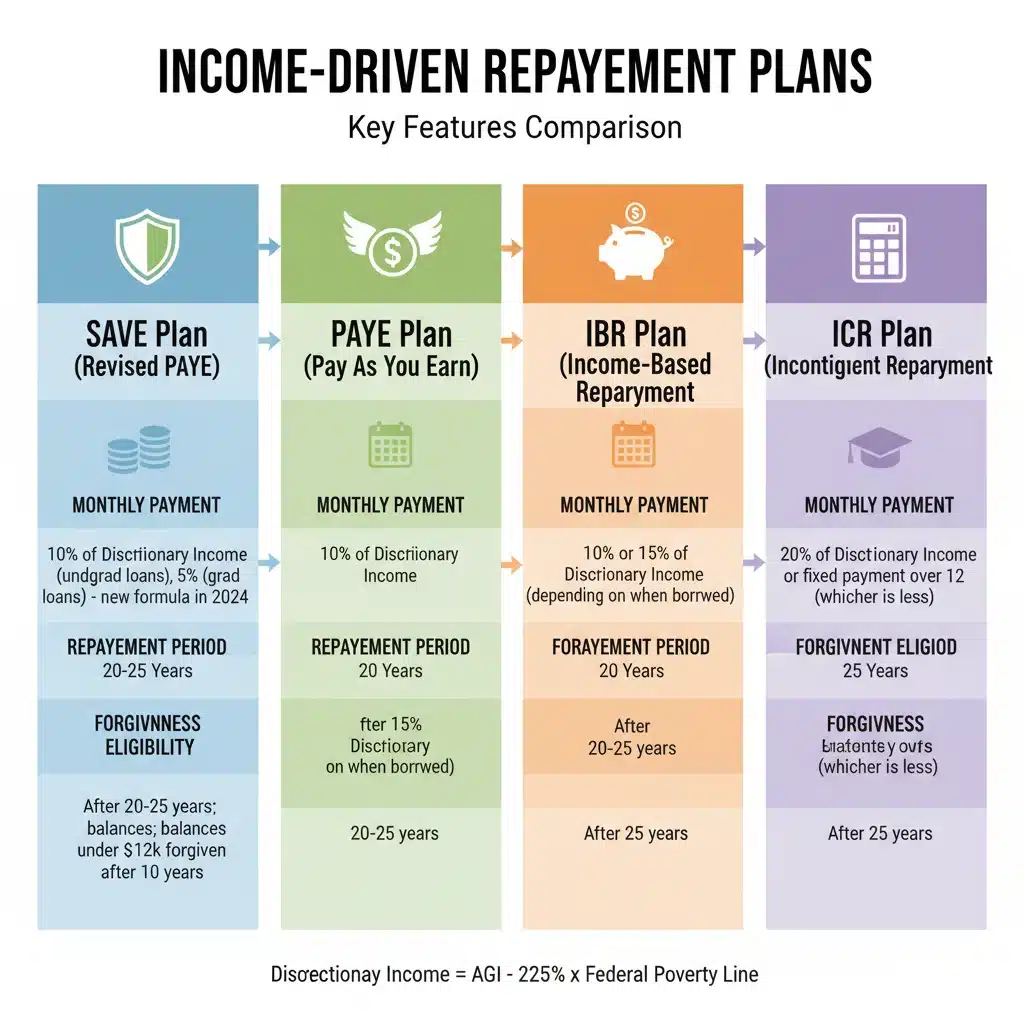

1. Saving on a Valuable Education (SAVE) Plan (formerly REPAYE)

The SAVE Plan is the newest and most beneficial IDR plan for many borrowers. Key features include:

- Payment Calculation: Your monthly payment is calculated based on 10% of your discretionary income. For undergraduate loans, this will drop to 5% starting July 2024.

- Discretionary Income Definition: Discretionary income is the difference between your adjusted gross income (AGI) and 225% of the federal poverty guideline for your family size. This is a more generous calculation than other IDR plans, meaning lower payments for most.

- Interest Subsidy: If your monthly payment doesn’t cover the full amount of interest due, the government covers the remaining interest, preventing your loan balance from growing due to unpaid interest. This is a significant benefit.

- Forgiveness: After 20 years of payments for undergraduate loans or 25 years for graduate loans, any remaining balance is forgiven.

The SAVE Plan is an excellent option for graduates with lower incomes relative to their loan balances, as it offers the potential for very low or even $0 monthly payments and prevents interest capitalization.

2. Pay As You Earn (PAYE) Repayment Plan

- Payment Calculation: Payments are generally 10% of your discretionary income.

- Discretionary Income Definition: Discretionary income is the difference between your AGI and 150% of the federal poverty guideline.

- Payment Cap: Your monthly payment will never be more than what you would pay under the Standard Repayment Plan.

- Forgiveness: After 20 years of payments, any remaining balance is forgiven.

PAYE can be a good option if you have a higher income but still want the flexibility of an IDR plan, especially if your income might increase significantly in the future, as the payment cap protects you from excessively high payments.

3. Income-Based Repayment (IBR) Plan

There are two versions of the IBR plan, depending on when you took out your first federal student loan:

- For new borrowers on or after July 1, 2014: Payments are 10% of your discretionary income, capped at the Standard Repayment Plan amount. Forgiveness after 20 years.

- For borrowers before July 1, 2014: Payments are 15% of your discretionary income, capped at the Standard Repayment Plan amount. Forgiveness after 25 years.

Discretionary income for IBR is calculated as the difference between your AGI and 150% of the federal poverty guideline.

4. Income-Contingent Repayment (ICR) Plan

The ICR Plan was the first IDR plan. It’s generally less generous than other IDR plans but can be an option if you don’t qualify for others or have Parent PLUS Loans (which can be made eligible for ICR through a Direct Consolidation Loan).

- Payment Calculation: Payments are the lesser of 20% of your discretionary income (AGI minus 100% of the federal poverty guideline) or what you would pay on a fixed 12-year repayment plan, adjusted according to your income.

- Forgiveness: After 25 years of payments, any remaining balance is forgiven.

Choosing the right IDR plan for your student loan repayment 2026 strategy requires careful consideration of your current income, expected future income, family size, and total loan balance. You can use the Loan Simulator on StudentAid.gov to compare different plans and see estimated monthly payments and total costs.

Public Service Loan Forgiveness (PSLF)

For 2026 graduates considering careers in public service, the Public Service Loan Forgiveness (PSLF) program is an extremely valuable benefit. PSLF forgives the remaining balance on your Direct Loans after you’ve made 120 qualifying monthly payments while working full-time for a qualifying employer. Qualifying employers include government organizations (federal, state, local, or tribal), non-profit organizations (501(c)(3) and others), and certain other non-profits that provide public services.

To qualify for PSLF, you must:

- Be employed by a U.S. federal, state, local, or tribal government or not-for-profit organization.

- Work full-time for that employer.

- Have Direct Loans (other federal loans can become eligible by consolidating them into a Direct Consolidation Loan).

- Repay your loans under an income-driven repayment plan.

- Make 120 qualifying monthly payments.

It’s crucial to submit an Employment Certification Form annually or whenever you change employers to ensure your payments are being counted towards PSLF. This proactive approach is key to a successful student loan repayment 2026 plan under PSLF.

Other Federal Loan Repayment Strategies

Loan Consolidation

A Direct Consolidation Loan allows you to combine multiple federal student loans into a single new loan with a single monthly payment. The interest rate is the weighted average of your original loans, rounded up to the nearest one-eighth of a percentage point. Consolidation can simplify your repayment and may allow you to access certain repayment plans (like some IDR plans or PSLF) that were not available for your original loan types (e.g., FFEL Program loans or Perkins Loans). However, consolidation can reset the clock on any payments made towards IDR forgiveness or PSLF, so weigh the pros and cons carefully.

Deferment and Forbearance

If you face temporary financial hardship, federal loans offer options to temporarily postpone your payments:

- Deferment: Allows you to temporarily stop making payments. For subsidized loans, interest typically does not accrue during deferment. Common reasons include unemployment, economic hardship, or returning to school.

- Forbearance: Allows you to temporarily stop or reduce your payments. Interest usually accrues on all loan types during forbearance, even subsidized ones. It’s often granted for financial difficulty, medical expenses, or other acceptable reasons.

While these options provide relief, they should be used judiciously, as accrued interest can add to your total loan cost.

Managing Private Student Loans

Private student loans offer fewer protections and repayment flexibilities compared to federal loans. However, 2026 graduates still have strategies to manage them effectively:

1. Refinancing Private Student Loans

Refinancing involves taking out a new loan from a private lender to pay off existing private (or even federal) student loans. The goal is typically to secure a lower interest rate, reduce your monthly payment, or change your loan term. This can be particularly beneficial if your credit score has improved since you first took out your loans or if you can qualify for a lower rate with a new lender.

Important consideration: Refinancing federal loans into a private loan means losing federal benefits like IDR plans, deferment, forbearance, and forgiveness programs. This decision should not be taken lightly.

2. Lender-Specific Hardship Programs

Some private lenders offer their own hardship programs, such as temporary payment reductions or deferment options. These are not standardized like federal programs, so you’ll need to contact your specific lender to inquire about their policies if you’re experiencing financial difficulty. This is a crucial step in any student loan repayment 2026 plan involving private loans.

3. Aggressive Repayment Strategies

If you can afford to, making extra payments on your private loans can save you a significant amount in interest over time, especially if you have high-interest variable-rate loans. Consider strategies like the debt snowball or debt avalanche method to prioritize your payments.

Tips for 2026 Graduates to Optimize Student Loan Repayment

1. Know Your Loans

The first step in any effective student loan repayment 2026 strategy is to know exactly what you owe. Gather information on all your loans, including:

- Loan type (federal or private)

- Loan servicer(s)

- Original principal balance

- Current balance

- Interest rate

- Repayment start date

You can find your federal loan information on StudentAid.gov. For private loans, check your credit report or contact your lenders directly.

2. Create a Budget

A realistic budget is the cornerstone of managing any debt. Track your income and expenses to understand how much you can comfortably afford to pay toward your student loans each month. Factor in other essential expenses like rent, utilities, food, and transportation, as well as savings goals.

3. Choose the Right Repayment Plan

Don’t default to the Standard Repayment Plan without exploring other options. Use the Loan Simulator to compare different federal plans. If you anticipate a lower starting salary, an IDR plan like SAVE might be your best initial choice. If your income is high and stable, the Standard Plan will save you money on interest.

4. Set Up Auto-Pay

Most loan servicers offer a small interest rate reduction (typically 0.25%) if you sign up for automatic payments. This not only saves you money but also ensures you never miss a payment, which is crucial for maintaining a good credit score.

5. Make Extra Payments (When Possible)

Even small extra payments can make a big difference over the life of your loan. If you receive a bonus, a tax refund, or have extra cash, consider applying it directly to your loan principal, especially on high-interest loans. Be sure to instruct your servicer to apply the extra payment to the principal, not to advance your due date.

6. Understand Loan Forgiveness and Discharge Options

Beyond PSLF, there are other situations where federal loans can be discharged or forgiven, such as Total and Permanent Disability (TPD) discharge, borrower defense to repayment, or closed school discharge. While these are for specific circumstances, it’s good to be aware of them.

7. Stay in Communication with Your Servicer

If you’re struggling to make payments, don’t ignore the problem. Contact your loan servicer immediately. They can inform you about options like changing your repayment plan, deferment, or forbearance. Proactive communication is always better than falling behind on payments.

8. Avoid Student Loan Scams

Be wary of companies that promise immediate student loan forgiveness or a quick fix for your debt for an upfront fee. Most legitimate services are free through the Department of Education or your loan servicer. Never pay for help that you can get for free.

Looking Ahead: Future Changes and Considerations

The student loan landscape is constantly evolving. As 2026 graduates, it’s important to stay informed about potential policy changes that could affect your student loan repayment 2026 plans. Keep an eye on announcements from the Department of Education and reliable financial news sources. For example, the SAVE Plan is still relatively new, and its full implementation and potential future adjustments will be important to monitor.

Furthermore, consider how your career path and life events might impact your repayment strategy. Getting married, having children, or pursuing further education can all affect your eligibility for certain plans or change your financial situation, necessitating a review of your repayment approach. Regularly reassess your financial situation and adjust your student loan repayment strategy as needed.

Conclusion

Navigating student loan repayment as a 2026 graduate is a significant undertaking, but it doesn’t have to be overwhelming. By understanding the differences between federal and private loans, exploring the various repayment plans (especially income-driven options like the SAVE Plan), and implementing smart financial habits, you can take control of your financial future. Remember to stay informed, maintain open communication with your loan servicers, and don’t hesitate to seek professional financial advice if you need personalized guidance.

Your journey after graduation is just beginning, and successfully managing your student loans is a critical step toward achieving your long-term financial goals. Equip yourself with knowledge, plan strategically, and you’ll be well on your way to financial independence.